Published on: February 19, 2025

Mumbai, 19th February, 25’: GroupM, WPP‘s media investment group in India, has released its latest report, “Profiling Cinemagoers,” which explores cinema viewing habits and their impact on consumer behavior across five key metropolitan cities: Bengaluru, Delhi, Pune, Mumbai, and Hyderabad. The study, conducted with a representative sample of 1,075 individuals aged 18-44, offers valuable insights into the shifting role of cinema as an entertainment and advertising medium.

The findings uncover intriguing cinema viewership trends, showcasing diverse audience behaviours. Heavy Viewers, watching 4+ movies monthly, represent 23% of respondents and emerge as the most engaged segment. Medium Viewers, who watch 2-3 movies per month, dominate the landscape at 57%, while Light Viewers, averaging 1 movie per month, account for the remaining 20%. This segmentation highlights the varied consumption patterns within the cinema audience, offering valuable opportunities for targeted engagement.

On average, people watch 18 movies annually, with men outpacing over women, pointing to a gender gap in viewership. Nearly a quarter of audiences enjoy the excitement of first day, first show screenings, while 42% watching movies on the release day. Evening screenings remain the top choice, and cinema continues to be a social activity for most, with 75% watching with family and friends, while some also enjoy it with colleagues, partners, or even alone.

Powered by ProCAT, a web-based platform that provides data-driven insights on cinema audiences, the report enables brands and advertisers to make informed decisions for targeted campaign planning.

Read full Report: Cinema eMailer 11Feb25 -Final[22]

Ajay Mehta, Managing Director, Cinema, OOH, and Experiential Marketing at GroupM, India, said,

“Cinema is not just an entertainment platform but a powerful medium for connecting with audiences.. This report underscores the relevance of cinema as a thriving entertainment and advertising platform. With 42% of viewers acknowledging the influence of cinema ads on their purchase decisions, it’s clear that the silver screen holds immense potential for meaningful consumer engagement. By understanding audience behaviour and preferences, we can empower advertisers to create impactful campaigns that resonate with cinema-goers and drive meaningful consumer engagement.”

Siddharth Bhardwaj, CEO of UFO Moviez India, added,

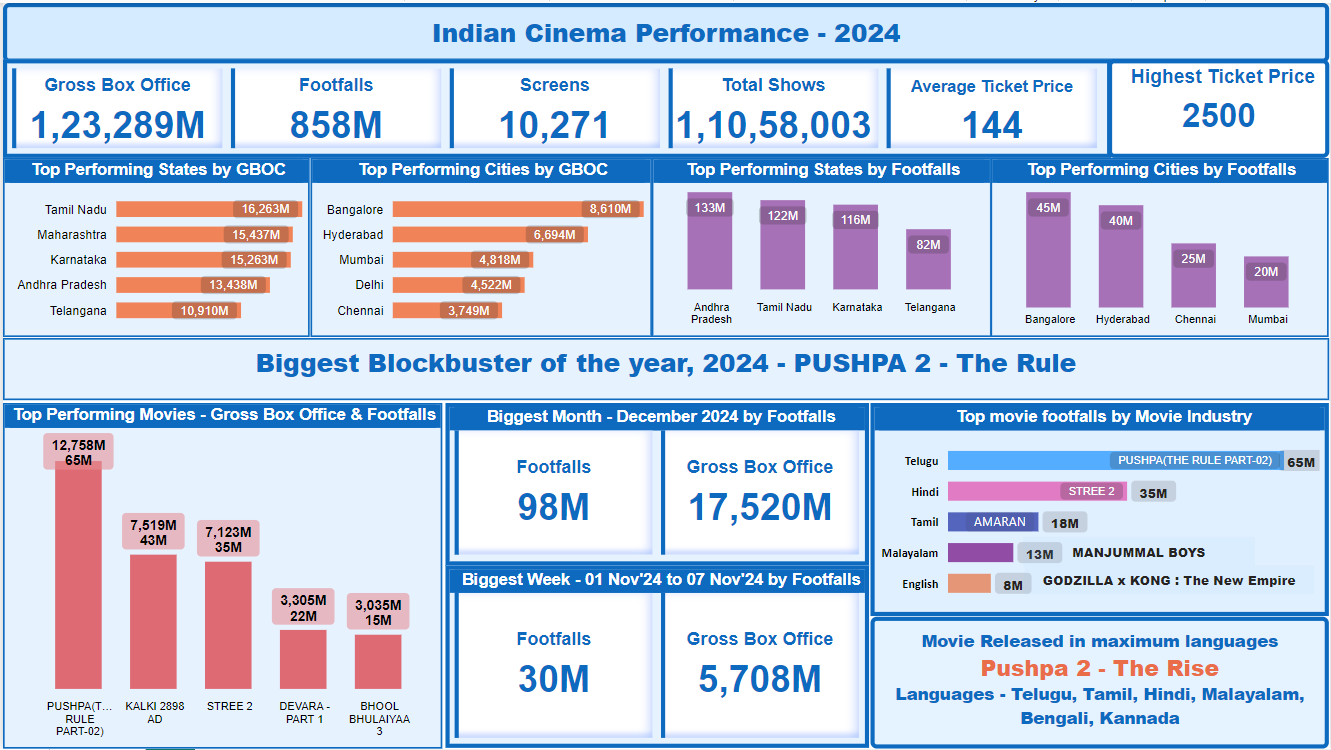

“With 858 million footfalls and a Gross Box Office Collection (GBOC) of ₹12.38 billion, cinema has emerged as a powerful driver of the ‘out-of-home economy.’ At UFO, data-driven strategies are at the heart of our offerings. Our platform, ProCAT, provides brands and advertisers with unparalleled insights into Indian cinema footfall trends, enabling precise campaign planning and performance evaluation. By leveraging historical data, guaranteed footfalls, and predictive admissions, advertisers can design highly targeted campaigns that captivate audiences in an immersive environment, maximizing engagement and ensuring a guaranteed return on investment.”

2024 Overview of Cinema Industry Trends:

The year 24’ revealed fascinating dynamics:

State & City Trends:

Kerala showed a 20%+ increase in box office collections. Andhra Pradesh and Telangana exhibited higher affinity for cinema relative to their population base. Bangalore and Hyderabad emerged as top contributors to gross box office collections. Mumbai and Chennai continued to have disproportionately high percentages of movie-goers.

Top Performing Metrics:

Gross Box Office (2024): ₹123B. Total Footfalls: 857M. Screens: 10,271. Average Ticket Price: ₹145. Month with Highest Footfall: December 2024 (97M footfalls, ₹1,746 Cr BO).

Record-Breaking Highlights:

Read more: Saatchi & Saatchi India brings alive the #FedExFactor in South Africa

![]()